IMA Analysis

Wednesday June 2, 2021

Developments in FinTech

IMA India Research Update June 2021

Despite Covid-19 – or perhaps thanks to it – India’s financial technology (FinTech) sector remains on a high growth trajectory. Propelling it forward are tailwinds such as strong consumer demand, an enabling regulatory environment, rich and diverse capital flows, a strong digital infrastructure backbone, and a large and relatively affordable tech talent pool. The sector’s high-velocity growth of the last five years is likely to continue over the next five as well. But the next round of growth will be more broad-based, with segments other than payments – the dominant category so far – gaining prominence. Several new trends will shape the industry, with ‘neo-banks’ gaining traction, micro-lending picking up, and hybrid banking becoming mainstream. The paper provides a perspective.

THE FINTECH LANDSCAPE: BRACING THE COVID IMPACT

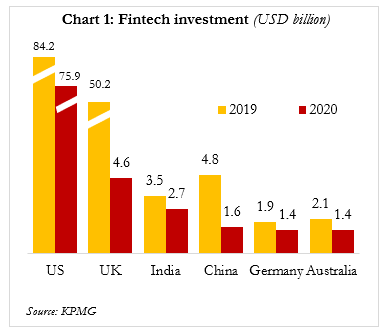

Despite Covid, India was among the top three FinTech investment destinations

India’s FinTech sector has seen exhilarating growth over the last few years, with start-ups dominating this space. Today, over 2,100 FinTech companies exist in India, ~70% of which have come up in the last 5 years. A recent FICCI-BCG report suggests that between 2016 and 2021, India’s FinTech sector received over USD 10 billion in investment – a figure that could more than double to USD 25 billion in the next four years. The study places the current net valuation of the sector at USD 50-60 billion.

Globally, FinTech investments were impacted… the UK and China were the worst affected and the US the least

Global FinTech investments were impacted last year by the pandemic. The US market stayed resilient, with USD 75.9 billion flowing in over the course of 2020, down from USD 84 billion the year before (Chart 1). The UK market was harder hit, with uncertainties around Brexit and the disproportionate impact of Covid-19 weighing on funding, which fell by over 90%. Meanwhile, inflows into India fell from a 2019 peak of USD 3.5 billion to USD 2.7 billion last year. However, with China seeing an even bigger drop, India displaced China to claim the third position globally. In part, China’s ‘decline’ reflects the relative maturing of its FinTech sector, particularly in the payments space, which is dominated by a small number of ‘mega giants’.

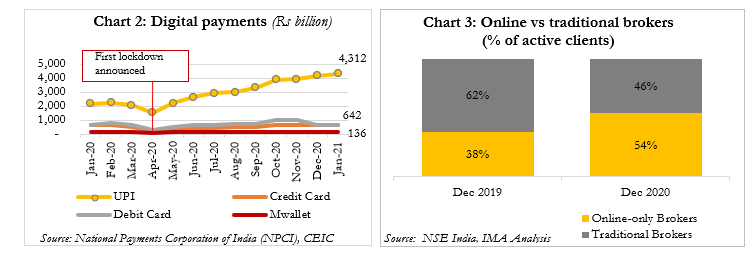

UPI payments surged to three times its pre-pandemic levels

Within India, Covid-19 slowed economic activity but accelerated digitisation. UPI payments surged, more than doubling in value in the 12 months to January 2021, while other forms of electronic payments stagnated (Chart 2). A similar acceleration was seen by online brokering firms such as Zerodha, Upstox, 5paisa and Groww, which gained a dominant position – 54% of active clients, up from 38% a year ago – by December 2020 (Chart 3).

OUTLOOK 2025

FinTech investments have become more broad-based

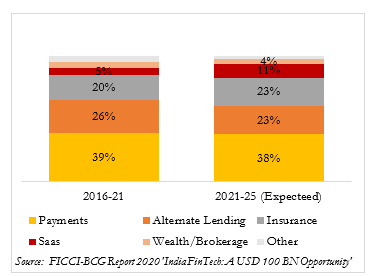

Given its relatively low base and assuming a reasonable ~20% CAGR, Indian FinTech is likely to be worth USD 100-150 billion by 2025. The sector’s diversity will add to its strength, with investment flows becoming more evenly spread across segments. The payments space, which attracted over 90% of investments in 2015, received just under 40% in the last five years – and this share is expected to remain stable through 2025 (Chart 4). Instead, the next wave of investments, almost 50%, is going towards companies engaged in alternative lending and insurance. InsureTech, in particular, has seen competition hotting up with incumbents enhancing their digital focus and new players entering. As noted above, FinTechs have already captured the lion’s share of the equity-brokerage market.

THE NEW FINTECH REVOLUTION: EMERGING TRENDS

As the FinTech landscape continues to evolve, a number of medium-term trends are becoming visible:

Virtual banks will become popular

- Neobanks could gain traction: A neobank is a completely virtual bank that provides personalised and seamless experiences and a user-friendly interface. Currently, there is no uniform regulatory structure around neobanks but in August 2019, the RBI introduced a new regulatory ‘sandbox’, providing a safe environment for FinTechs to test and experiment with new financial technologies in a controlled environment. Over a dozen neobanks have come up in the last few years, including SBI’s Yono, Kotak’s 811, RazorpayX, Open and NiYo. Most of these work in partnership with traditional banks. With Covid-19 pushing up the need for contactless and faceless banking, further policy/regulatory advances in this area should be expected.

Huge opportunity in the alternate lending space

- Micro-lenders will mushroom: One of FinTech’s biggest advantages is that it can enable the end-to-end digital processing of transactions at low cost. This is particularly important in areas such as micro-lending to small businesses and individuals. Not surprisingly, in 2020, more than a quarter of the USD 2.7 billion in funding to FinTech was garnered by consumer and B2B lending start-ups like MoneyTap and Capital Float.

More aggregator platforms will emerge

- Fin-sec aggregators will gain market share: Loan and insurance aggregators such as PolicyBazaar, PaisaBazaar and Coverfox gained traction in 2020. Their biggest attraction is that they enable users to compare and contrast policy prices and features, loan rates and even after-sales metrics such as claim ratios. Detailed usage data are not available in the public domain but it is clear, following the ‘money trail’, that investors see merit in this segment. In FY21, they pumped over USD 120 million into PolicyBazaar (the first unicorn in this segment) and close to USD 100 million in Digit Insurance (the second).

Greater consolidation in the banking space

- Hybrid banking will become mainstream: In the last few years, the RBI has made concentrated efforts to get institutional banks to digitise while penalising banks that fall short on technical standards. A case in point is its recent halting of all new digital launches by HDFC Bank after it suffered a series of server outages. This regulatory push is likely to drive banks to seek partnerships within the start-up ecosystem that will help them streamline their digital banking operations and widen their offerings. For instance, HDFC Bank bought a stake in FinTech start-up ‘Smallcase’, an online investment management player. Both Kotak and HDFC have purchased stakes in Ferbine, an online retail payment system, and ICICI Bank in two fintech firms, City Cash (transit payments) and Thillais Analytical Solutions (neobanking). This suggests that hybrid banking, led by consolidation within FinTech, will be a key theme this year and beyond.

THE REGULATORY LANDSCAPE: GAPS AND OPPORTUNITIES

Multiple bodies regulating the FinTech space

Like the financial sector itself, India’s FinTech space is regulated by multiple agencies, including the RBI, SEBI, IRDA and TRAI. Further, each state has its own policies on the start-up ecosystem, which results in overlaps, contrasting views and several grey areas. A welcome development was the aforementioned setting up, under the RBI’s Inter-Regulatory Working Group on FinTech and Digital Banking, of a regulatory ‘sandbox’ along the lines of those established by the Monetary Authority of Singapore and the UK’s Financial Conduct Authority. This approach allows FinTech start-ups to test out new services and assess risks before they are taken to market. Crucially, FinTech firms and regulators can work together to tweak existing regulations, enabling firms to test their products for a limited time and among a limited number of customers.

Recent moves in the payments space show regulatory intent to bolster the segment

Recent regulatory measures by the RBI aim to bolster India’s digital infrastructure and enable a level playing field in the payments space. In June 2020, it announced the creation of a Payments Infrastructure Development Fund (PIDF) to encourage firms to deploy Points of Sale (PoS) channels (both physical and digital) across the country to improve the penetration of card-based and other digital payments. In August 2020, it released a draft framework for setting up a New Umbrella Entity (NUE) for retail payments. NUEs can be established either as a for-profit or not-for-profit company, and will be permitted to set up ATMs, offer white-label POS terminal services, undertake Aadhaar-based payments and remittances, and develop other new payment solutions.

The broader FinTech regulatory landscape must evolve to address long-term growth prospects

As the industry matures, the regulatory landscape must also evolve, taking on a broader and deeper mandate. The industry itself will need to address some concerns that could, if not dealt with early on, limit its longer-term growth prospects:

- Data privacy: Misuse of consumer data is widely prevalent and FinTechs must adhere to the highest standards of data security, privacy and consent-based access.

- Data security: In the wake of rising cyber-attacks, businesses must adopt best-in-class practices to protect customer assets.

- Risk frameworks: FinTechs must adhere to the same enterprise risk standards as their established larger counterparts in the traditional financial services space.

|

This paper has been produced by IMA’s in-house research team based on desk research and conversations with CXOs from the FinTech sector. This paper is meant for the exclusive consumption of IMA’s Peer Group Forum members and may not be copied, shared or distributed without explicit permission. Please visit www.ima-india.com to view current papers and our full archive of research content in the IMA members’ Knowledge Centre, accessible via the Login link on top of the page. A podcast version of this paper is also available there. IMA Forum members have personalised website access codes. |

Copyright ©️ 2021-22 INTERNATIONAL MARKET ASSESSMENT INDIA PRIVATE LIMITED. All rights reserved